How to Prepare for Mandatory Digital Compliance

Across the European Economic Area, the adoption of electronic invoicing is advancing rapidly. What began as a digitalization initiative has progressed into an operational requirement. As governments intensify efforts to reduce the Value-added Tax (VAT) gap, strengthen tax transparency, and improve cross-border efficiency, e-invoicing compliance is becoming mandatory in more European countries each year. If your organization issues or receives business-to-business (B2B) invoices in Europe, now is the time to prepare for the shift to digital invoicing.

This article covers what a compliant electronic invoice (e-invoice) is, how e-invoicing regulations are unfolding across countries, and the steps businesses should take to prepare.

What Electronic Invoicing Means in Europe

In the European regulatory context, an electronic invoice must be issued, transmitted, and received in a structured format. This structured format is based on EN 16931, the European semantic model defined under the EU e-invoicing directive, which defines the core information elements required for interoperability across borders and industries.

This semantic standard ensures that all e-invoices can be validated, interpreted by systems, and exchanged reliably, allowing automated checks, accurate VAT handling, and efficient invoice processing from creation through archiving.

This standardization is key for the continent-wide shift to real-time reporting. Countries rely on approved syntaxes and shared networks, such as Pan-European Public Procurement Online (Peppol), to ensure e-invoices can move securely between suppliers, buyers, and mandated government platforms.

For businesses, this means electronic invoicing solutions must generate fully-structured invoice data, apply all relevant rules, validate mandatory fields, and securely transmit information. The result? A more accurate, automated, and unified digital invoicing environment.

Why Europe is Accelerating Digital Invoicing

The acceleration is driven by the combined goals of tax modernization, fraud reduction, and improved economic efficiency. Governments gain clearer visibility of taxable transactions, reducing errors and inconsistencies. Key e-invoicing benefits are increasingly recognized across industries.

Businesses benefit from the operational advantages of structured e-invoicing: faster processing, fewer disputes, improved auditability, and enhanced cash-flow management.

Structured digital invoicing eliminates manual steps and supports automated reconciliation, helping organizations achieve higher first-time acceptance rates and more reliable payment cycles. As a result, complying with e-invoicing regulations becomes not just a requirement but a driver for stronger financial performance.

Europe’s E-Invoicing Requirements

European e-invoicing regulations are anchored in EU-level standards but implemented through national mandates. Directive 2014/55/EU, commonly referred to as the EU e-invoicing directive, required public sector entities to receive and process invoices that comply with EN 16931. It has significantly influenced the private sector, prompting many EU countries to introduce mandatory B2B e-invoicing requirements based on the same EN 16931 technical standard. Most Member States have already adopted business-to-government (B2G) electronic invoicing, and many are progressing toward B2B mandates that will become compulsory by 2028.

Countries are deploying different compliance models:

- Clearance models. Tax authorities validate e-invoices before reaching the buyer.

- Continuous Transaction Controls (CTC). These require near real-time reporting.

- Post-audit models. Reporting occurs after transactions.

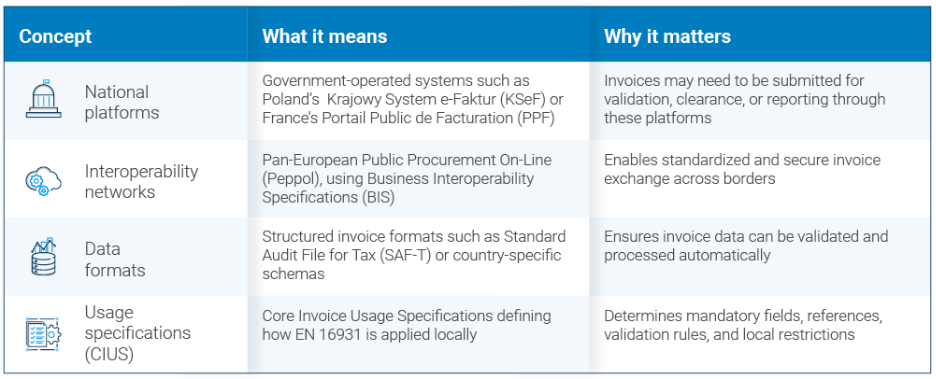

Although Europe is moving towards a harmonized approach to electronic invoicing, the way requirements are implemented still varies by country. Most national frameworks combine government platforms, shared interoperability networks, and local usage rules, all built on the European EN 16931 standard. For organizations, compliance depends on understanding not just invoice content, but also how and where invoices must be transmitted.

Together, these elements define what invoice data must be sent, how it must be structured, which network or platform must be used, and which business rules apply in each country.

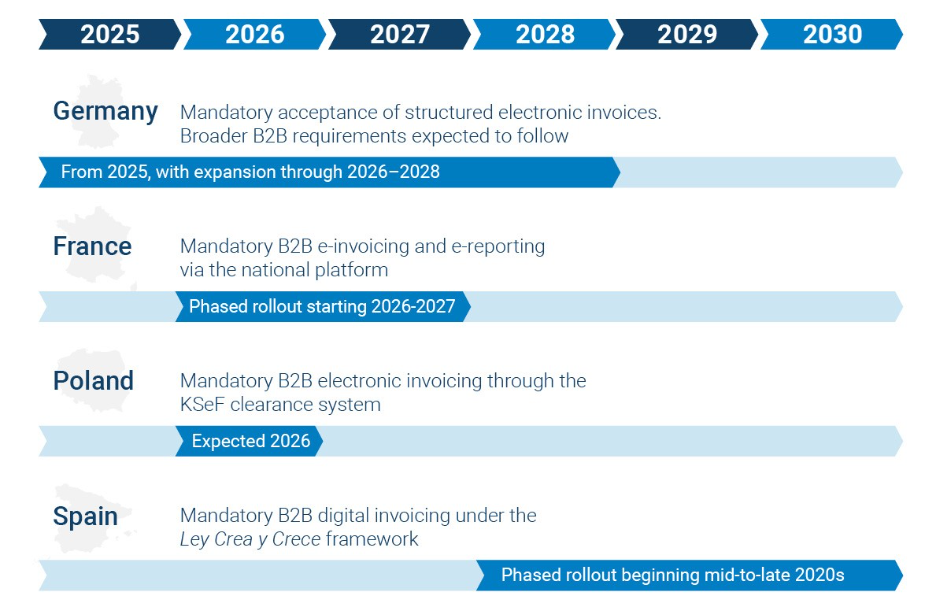

Upcoming E-Invoicing Deadlines in Europe

While timelines vary, several major European economies are entering critical implementation phases, such as Belgium, where e-invoicing via Peppol became mandatory in January 2026. These deadlines are particularly relevant for organizations issuing or receiving B2B invoices:

Check out the dates and requirements for other European countries on our interactive map.

Four Steps to Prepare for Mandatory E-Invoicing

Rolling out electronic invoicing across Europe involves both technical and organizational change. To prepare effectively, companies need a structured approach that brings together finance, IT, tax, and procurement teams and reduces the risk of disruptions as mandates take effect across Europe. Here are four simple steps to prepare for e-invoicing:

Finance and tax teams should review invoice content against the European EN 16931 standard and applicable national requirements. This includes validating supplier and customer records, VAT IDs, addresses, and tax rates. Gaps in data quality are a major cause of invoice rejection, delays, and penalties, so remediation at this stage is critical to ensure every electronic invoice can be processed successfully.

Once data is aligned, businesses must ensure invoices can be exchanged through the correct channels. This may involve enabling connectivity to interoperability networks such as Peppol, integrating with national platforms, or supporting multiple transmission models at the same time. Secure APIs, reliable delivery, and certified connectivity, provided by an experienced e-invoicing provider, are key to meeting local and cross-border requirements.

E-invoicing works best when compliance is embedded directly into Enterprise Resource Planning (ERP) and finance applications. This supports automated reconciliation, reduces manual intervention, and enables organizations to manage different compliance models across countries.

E-invoicing compliance is not a one-time project. Regulations, schemas, and business rules continue to change, requiring ongoing maintenance. Companies should establish clear ownership across finance, tax, and IT, monitor regulatory updates, and schedule testing. Supplier enablement and training also play a key role in sustaining compliance as mandates expand.

Compliance is just the beginning

The EU’s VAT in the Digital Age (ViDA) agenda will further synchronize and expand digital invoicing and digital reporting requirements. Businesses should expect extended B2B mandates, expanded real-time reporting, and a more unified approach to interoperability.

By 2030, mandatory e-invoicing is expected to be widespread across the EU, and organizations with robust, flexible e-invoicing software will be able to adapt quickly as new obligations emerge to capture long-term e-invoicing benefits and avoid any operational disruptions.

Descartes can help you build a scalable, secure environment for exchanging structured e-invoices across multiple countries. Our e-invoicing solutions validate data against European and national specifications, integrate seamlessly with ERP systems, and connect to mandated frameworks and clearance models, such as Peppol or the Polish KSeF platform, and others, helping organizations stay aligned with e-invoicing regulations.

If you are starting your journey to e-invoicing compliance today or if you wish to re-evaluate your current solution provider, reach out to one of our experts!

Would you like to learn more about E-Invoicing solutions ?

More E-Invoicing Resources