The Global Shipping Report

December U.S. Container Imports Post Small Month-over-Month Increase, Closing 2025 Just Under 2024 Totals

Stay informed with the latest insights from the Descartes Global Shipping Report

Data for the Global Shipping Report provided by Descartes Datamyne

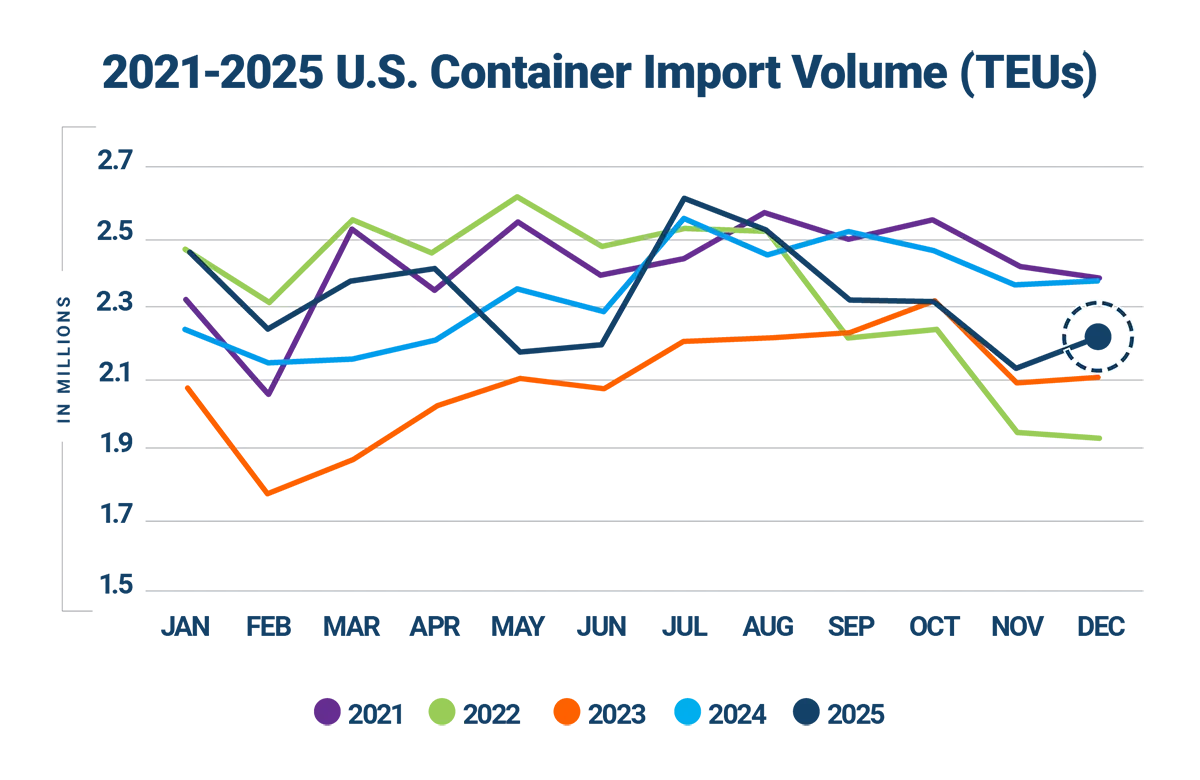

In December 2025, U.S. container imports totaled 2,227,316 twenty-foot equivalent units (TEUs), increasing 2% from November. Despite the small month-over-month increase, year-over-year imports declined and full-year totals ultimately finished 0.4% below 2024 levels, as the suspected early-year frontloading gave way to slower growth, shifting sourcing patterns, and persistent policy uncertainty. China-origin imports continued to weaken in December, while Southeast Asian countries gained share, partially offsetting declines across the top countries of origin (CoO).

Operational conditions improved across East and Gulf Coasts ports, while West Coast transit times saw minimal overall change. At the same time, West Coast ports expanded their share of U.S. imports while East and Gulf Coast volumes moved lower. On the policy front, delayed tariff increases and scaled-back trade actions provided limited near-term relief, but broader uncertainty—including U.S.–China trade tensions, ongoing Red Sea disruptions, and elevated geopolitical risk tied to developments in Venezuela —continues to shape the global shipping environment entering 2026.

In this Article...

- U.S. container imports reached 2,227,316 TEUs in December 2025.

- December 2025 imports increased by 2% over November and were 5.9% lower than December 2024.

- December 2025 imports from China were 705,789 TEUs, down 1% from November and 31% below the record high of 1,022,913 TEUs set in July 2024.

- December 2025 U.S. imports from the top 10 countries of origin increased by 1.9% over November, led by gains from Vietnam and South Korea.

- In December 2025, West Coast ports grew their lead in market share, while the share at East and Gulf Coast ports contracted.

- December 2025 port delays improved across East and Gulf Coast gateways, while West Coast transit times showed minimal change and no signs of broad congestion.

- The U.S. delayed planned tariff increases on furniture and cabinet imports, providing temporary tariff relief.

- Developments in Venezuela add to broader geopolitical uncertainty affecting global trade flows.

- Red Sea security risks persist, with most carriers continuing to reroute around the Cape of Good Hope and extended transit times remained the norm.

- Key points to monitor and manage supply chain risks.

- Recommendations to help mitigate global shipping challenges.

U.S. container imports finish 2025 slightly below 2024 levels.

U.S. container import volumes totaled 2,227,316 TEUs in December 2025, a 5.9% decline compared with December 2024 (see Figure 1). Despite periods of strength earlier in the year, total 2025 import volumes finished 0.4% below 2024, reversing what had been nearly 10% year-over-year growth at the start of the year. This gradual softening likely reflects a combination of frontloaded shipments in early 2025, a cooling economic environment, and easing consumer demand, which collectively narrowed and ultimately eliminated annual container import growth.

Figure 1: U.S. Container Import Volume Year-over-Year Comparison

Source: Descartes Datamyne™

December 2025 import volumes rose 2% from November, an increase of 44,268 TEUs (see Figure 2), ranking as the second-largest month-over-month gain for December over the past decade. While December coincides with the U.S. holiday period, the month does not typically experience pronounced shifts in import volumes, as the primary seasonal slowdown generally occurs in November with activity declining through December. Against that seasonal backdrop, December 2025 still stands as the fourth-strongest December on record, trailing only 2020, 2021, and 2024, highlighting the continued resilience of U.S. import demand despite ongoing policy and economic uncertainty.

Figure 2: November to December U.S. Container Import Volume Comparison

Source: Descartes Datamyne™

Top 10 U.S. port volumes rebound modestly in December.

After the typical seasonal slowdown in November, container volumes across the top 10 U.S. ports increased by 35,853 TEUs in December 2025, a 2.0% month-over-month gain (see Figure 3). Performance across individual ports was mixed. Los Angeles recorded the largest increase, rising 9.2% (35,948 TEUs), while Oakland increased 7.3% (5,024 TEUs) and Long Beach posted a more modest 2.2% gain (8,365 TEUs). On the East Coast, some ports saw incremental growth, including Savannah (1.7%), Charleston (4.0%), and Norfolk (1.5%), while Philadelphia surged 32.4% (11,263 TEUs), marking the strongest percentage increase among major gateways. Not all ports participated in the rebound. New York/Newark declined 7.6% (24,652 TEUs), alongside smaller pullbacks in Houston (5.2%) and Tacoma (3.1%). Overall, the modest December increase aligns with typical seasonal patterns.

Figure 3: November 2025 to December 2025 Comparison of Import Volumes at Top 10 U.S. Ports

Source: Descartes Datamyne™

China-origin import volumes continue to decline in December.

U.S. containerized imports from China totaled 705,789 TEUs in December 2025, down 1.0% month-over-month, 21.8% year-over-year (see Figure 4), and 31% below the July 2024 peak. China’s share of total U.S. container imports eased further to 31.7%, continuing the gradual decline observed throughout 2025. At 31.7%, China’s share of total U.S. container imports in December 2025 is the lowest compared to the same month in each of the last six years (Dec. 2019: 38.5%, Dec. 2020: 41.6%, Dec. 2021: 41.8%, Dec. 2022: 35.6%, Dec. 2023: 37.4%, Dec. 2024: 38.1%).

China’s import mix in December remained concentrated in consumer goods and industrial inputs. Furniture and bedding (HS-94) remained the largest category at 115,353 TEUs, accounting for 16.4% of China-origin imports, followed closely by plastics (HS-39) at 15.6%. Machinery (HS-84) and electrical machinery (HS-85) together represented 19.0% of total China-origin volumes, while toys and sporting goods (HS-95) accounted for 5.8%. Apparel categories remained relatively small contributors, with knit apparel (HS-61) and non-knit apparel (HS-62) together comprising just 3.0% of China-origin imports. Overall, December’s category distribution underscores the continued shift in China-origin trade toward a narrower mix of goods, as policy pressures, sourcing diversification, and softer demand continue to weigh on volumes.

Figure 4: December 2024–December 2025 Comparison of U.S. Total and Chinese TEU Container Volume Relative to Chinese Import Record

Source: Descartes Datamyne

China-origin imports ease slightly across key U.S. ports in December.

In December 2025, China-origin container volumes across the top 10 U.S. ports declined by 5,592 TEUs, a 0.8% month-over-month decrease (see Figure 5). Port-level performance was mixed. Los Angeles recorded the largest increase, rising 6.2% (10,451 TEUs), Charleston increased 19.5% (3,813 TEUs), Norfolk 11.2% (2,037 TEUs), Oakland 7.1% (1,985 TEUs), and Savannah 1.3% (826 TEUs). Declines were concentrated at New York/Newark, which fell 11.0% (9,354 TEUs), Houston 13.2% (5,117 TEUs), Tacoma 10.1% (2,503 TEUs), Seattle 11.5% (1,403 TEUs), and Long Beach 3.0% (6,329 TEUs). Overall, December’s modest pullback reflects uneven but generally stable China-origin volumes, rather than the broad-based contraction observed in November.

Figure 5: November 2025 to December 2025 Comparison of top U.S. Ports for Imports Originating from China

Source: Descartes Datamyne

Top CoO volumes increased modestly in December amid mixed country-level performance.

In December 2025, U.S. containerized imports from the top 10 countries of origin increased 1.9% month-over-month, with a combined gain of 28,356 TEUs (see Figure 6). Growth was led by Vietnam, which rose 5.6% (14,711 TEUs), and South Korea, which increased 16.6% (12,991 TEUs). Taiwan also posted a strong gain of 14.1% (6,763 TEUs), Italy increased 7.8% (4,192 TEUs), Thailand 2.6% (2,856 TEUs), Indonesia 2.3% (1,304 TEUs), and Japan 2.1% (1,081 TEUs). Declines were concentrated in three countries: China decreased 1.0% (7,342 TEUs), India 5.9% (5,371 TEUs), and Hong Kong 4.3% (2,831 TEUs). Overall, December’s modest increase reflects broad stabilization across major sourcing countries, with gains outside China offsetting continued softness in China-origin volumes.

Figure 6: November 2025 to December 2025 Comparison of U.S. Import Volumes from Top 10 Countries of Origin

Source: Descartes Datamyne

China-driven weakness continues to weigh on year-over-year CoO volumes.

In December 2025, U.S. containerized imports from the top 10 countries of origin declined 8.4% year-over-year, with a combined decrease of 143,200 TEUs (see Figure 7). The contraction was driven primarily by China, which fell 21.8% (196,730 TEUs) and accounted for more than the total net decline. Additional year-over-year decreases were recorded from India (15.0%), Taiwan (13.2%), South Korea (7.1%), and Italy (1.0%). In contrast, several Southeast Asian origins posted strong year-over-year growth. Thailand increased 28.3% (24,511 TEUs), Vietnam 21.5% (48,889 TEUs), and Indonesia 19.6% (9,527 TEUs). More modest gains were recorded from Japan (1.7%) and Hong Kong (1.1%). Overall, December’s results highlight the ongoing divergence in sourcing patterns, with expanding volumes from Southeast Asia partially offsetting sustained weakness in China-origin imports, but not enough to reverse the broader year-over-year decline among top CoO.

Figure 7: December 2024 to December 2025 Comparison of U.S. Import Volumes from Top 10 Countries of Origin

Source: Descartes Datamyne™

West Coast port share rises in December, while East and Gulf Coast share eases.

In December 2025, U.S. container import shares shifted modestly from November levels (see Figure 8). West Coast ports increased their share to 44.0%, up from 42.6% in November, extending the lead they have maintained since mid-2025. In contrast, East and Gulf Coast ports accounted for 39.3% of total volumes, down from 41.1% the prior month. The top 10 U.S. ports handled 83.3% of total containerized imports, slightly below 83.8% in November. Overall, month-to-month changes remained limited, with coast-to-coast shares staying within the typical range observed throughout the year, underscoring a broadly stable national distribution of import flows despite modest regional shifts.

Figure 8: Volume Analysis for Top Ports, West Coast Ports and East and Gulf Coast Ports

Source: Descartes Datamyne™

East and Gulf Coast port delays improve in December, with minimal change across West Coast gateways.

In December 2025, average port transit time delays declined across most East and Gulf Coast ports compared with November (see Figure 9). New York/New Jersey recorded the largest improvement, with delays falling 1.5 days, while Savannah decreased 0.7 days, Norfolk declined 0.9 days, and Charleston improved 0.9 days. Houston was the exception, with delays increasing 0.7 days. On the West Coast, transit times were largely unchanged overall, with Los Angeles holding steady, Oakland remaining flat, and Long Beach easing slightly by 0.5 days. Tacoma and Seattle posted modest increases. Overall, December’s results indicate improvement across East and Gulf Coast gateways, while West Coast conditions remained relatively stable, with no signs of broad congestion.

Figure 9: Monthly Average Transit Delays (in days) for the Top 10 Ports (Oct. 2025 – Dec. 2025)

Source: Descartes Datamyne™

Note: Descartes’ definition of port transit delay is the difference as measured in days between the Estimated Arrival Date, which is initially declared on the bill of lading, and the date when Descartes receives the U.S. Customs and Border Protection (CBP) processed bill of lading data.

Trusted by

Stay informed with monthly shipping insights with the Global Shipping Report

Director, Industry Strategy, Global Trade Intelligence, Descartes

Gulf Coast import volumes remain soft.

In December 2025, Gulf Coast container imports totaled 199,933 TEUs, essentially flat month- over-month following November’s decline (see Figure 10). Additionally, December volumes remained 10.2% below the rolling 12-month average of 222,561 TEUs, indicating continued softness relative to recent levels. While the pace of decline slowed in December, Gulf Coast import activity has yet to regain momentum following mid-year volatility, with volumes remaining below trend as the year closed.

Figure 10: January 2025 to December 2025 U.S. Gulf Coast Container Imports

Source: Descartes Datamyne™

Venezuela developments elevate geopolitical risk, with indirect implications for U.S. trade.

In early January 2026, a U.S. military operation in Venezuela resulted in the capture of President Nicolás Maduro and his wife, who were transported to the United States to face long-standing federal criminal charges. While Venezuela is not a major source of U.S. containerized imports, the action has elevated geopolitical uncertainty in the region. This may indirectly affect global logistics conditions through energy market volatility, sanctions compliance challenges, and heightened regional risk premiums, which can influence fuel costs, insurance rates, and broader supply chain planning, even if direct impacts on U.S. import volumes remain limited at this time.

U.S. delays higher furniture tariffs, easing near-term pressure on imports.

In late December 2025, the U.S. administration postponed planned tariff increases on imported upholstered furniture, kitchen cabinets, and vanities for one year, keeping current tariff rates in place instead of allowing higher duties to take effect on January 1, 2026. The existing 25% tariff remains, while the scheduled increases to 30% (furniture) and 50% (cabinets and vanities) are now delayed until at least January 1, 2027 under the proclamation signed on December 31, 2025. This move provides short-term relief for importers and retailers that rely on these goods, which are often sourced from major exporters including China and Vietnam, but broader tariff uncertainty continues to affect U.S. import planning and costs.

U.S. scales back proposed tariffs on Italian pasta imports.

In early January 2026, the U.S. Department of Commerce significantly reduced previously proposed anti-dumping tariffs on Italian pasta imports after a preliminary review, lowering duties that had been slated to reach historically high levels. Originally, additional import duties upwards of 92–107% had been proposed on 13 Italian producers following an investigation into alleged below-market pricing, a move that raised concerns about sharply higher costs for U.S. importers and consumers. After reassessing producer responses and cooperation, the department cut the provisional duties with a final determination now scheduled for March 2026. This change reduces the risk of severely elevated tariffs on a product category valued at roughly $800 million in U.S. imports and reflects ongoing trade policy recalibration at the start of the year.

U.S.–China trade measures remain unchanged, with longer-term risks still in focus.

Recent U.S. and China policy actions, including extended Section 301 tariff exclusions and limited adjustments to export controls, continue to shape near-term trade conditions. However, there were no material changes in December, and the broader tariff framework and underlying disputes remain unresolved. As a result, the outlook remains uncertain, and U.S.–China trade policy developments continue to warrant close monitoring.

Liberation Day tariffs remain in effect as legal challenge continues.

The Liberation Day tariffs remain in force, with legal challenges to their implementation under the International Emergency Economic Powers Act (IEEPA) still unresolved. There were no material developments during December, and no ruling has altered current enforcement. As a result, importers continue to operate under elevated policy uncertainty, and the situation remains one to monitor rather than a source of near-term change.

Red Sea rerouting remains largely unchanged as carriers proceed cautiously.

While a small number of limited Red Sea and Suez Canal transits have resumed on a trial basis, the majority of container shipping lines continue to avoid the corridor. Broader returns remain unlikely in the near term, as carriers and insurers still require stronger and more consistent security assurances. As a result, Cape of Good Hope rerouting, longer transit times, and elevated costs remain the prevailing operating environment, with no material shift observed since last month.

Managing supply chain risk: what to watch in 2026.

In December 2025, U.S. container imports increased modestly from November to 2.23M TEUs, reflecting typical seasonal stabilization following November’s sharper slowdown, though volumes remained 5.9% lower year-over-year. China-origin imports continued to weaken, declining 1.0% month-over-month and remaining well below prior-year and peak levels. Recent trade policy actions, including delayed tariff increases on furniture and cabinets and scaled-back proposed duties on Italian pasta, provided limited near-term relief, while broader U.S.–China trade measures and Liberation Day tariffs remained unchanged, sustaining longer-term policy uncertainty. Globally, Red Sea security risks persist, keeping most container services rerouted around the Cape of Good Hope and maintaining extended transit times and elevated costs. Taken together, these dynamics point to a cautious global trade environment entering early 2026, shaped more by risk management than by clear growth momentum. Here’s what Descartes is monitoring in the months ahead:

- Expanded tariffs and other potential ‘protectionist’ trade policies. Broader and deeper tariffs applied to a wide array of goods could compel U.S. importers to significantly re-engineer their supply chains, putting additional pressure on global logistics infrastructure. While China-origin imports continued to decline into December, importers remain focused on evolving tariff policy. Recent U.S. actions, including extended Section 301 exclusions, the delay of higher tariffs on furniture and cabinets, and scaled-back proposed duties on Italian pasta, have provided limited, near-term relief, but longer-term uncertainty persists around technology restrictions, subsidies, and market access. At the same time, Liberation Day tariffs remain in force pending Supreme Court review, and the reciprocal tariff framework enacted in August continues to impose duties ranging from 10% to 41% on goods from more than sixty trading partners, keeping tariff risk a central and ongoing consideration in supply chain planning.

- Monthly TEU volumes between 2.4M and 2.6M. This level has historically been a key pressure point for U.S. ports and inland logistics networks. December 2025 import volumes increased modestly to 2.23M TEUs, but remained well below the 2.4M–2.6M TEU range associated with heightened congestion risk. While volumes stabilized following November’s seasonal slowdown, the continued gap reflects tempered demand and cautious importer behavior, rather than capacity-driven constraints, suggesting limited near-term pressure on port and inland transportation systems.

- Port transit wait times. If they decrease, it’s an indication of improved global supply chain efficiencies or that the demand for goods and logistics services is declining. In December 2025, transit delays declined across most East and Gulf Coast ports, while West Coast transit times showed minimal overall change. There were no indications of widespread congestion, pointing to generally balanced port operations.

- The economy. The U.S. is an import-driven economy, so economic health is an important indicator of container import volumes. The U.S. economy continues to show mixed signals that could influence import demand. At its December 9–10 meeting, the Federal Reserve cut the federal funds rate by 25 basis points to a range of 3.50–3.75%, marking the third rate reduction in 2025 as policy makers weighed cooling labor market indicators against persistently elevated inflation pressures. Labor market conditions remain uneven, with hiring moderating and unemployment holding near multi-year lows, while manufacturers report ongoing contraction. Any softening economic backdrop may temper U.S. import volumes, as demand and business investment adjust to slower growth and higher costs.

- Middle East conflict. Although attacks have eased, security risks in the Red Sea remain, and most major carriers continue to avoid Suez transits. Industry updates show that operators are unlikely to reverse Cape of Good Hope detours without stronger safety assurances, keeping longer transit times and elevated costs in place for now.

Consider recommendations to help minimize global shipping challenges.

December 2025 import volumes increased modestly from November but closed the year slightly below 2024 levels, reflecting a shift from early-year frontloading to a more cautious demand environment. While port operations remained generally stable, ongoing tariff uncertainty, uneven sourcing shifts, and prolonged Red Sea rerouting continue to complicate planning for importers. Recent U.S. trade policy actions have provided limited, short-term relief, but longer-term risks remain unresolved amid a cooling economic backdrop. Descartes continues to monitor these conditions through Descartes Datamyne™, government releases, and industry intelligence to help importers anticipate disruptions, optimize logistics performance, and strengthen supply chain resilience in an increasingly complex global trade environment.

Short-term:

- Monitor developments in Venezuela and related sanctions enforcement, particularly for potential indirect impacts on energy markets, compliance requirements, fuel costs, and regional shipping risk.

- Model the effects of the U.S.–China trade framework, including reduced tariffs on Chinese goods and suspended retaliatory measures, while also accounting for uncertainty tied to Liberation Day tariff litigation.

- Monitor port volumes and delays to assess the possibility of trade disruptions if volumes persist within the 2.4M and 2.6M levels that have historically stressed U.S. maritime logistics infrastructure.

- Track the Middle East conflict as carriers continue to avoid the Red Sea due to Houthi attacks, and heightened Iran–Israel tensions, with rerouting expected to persist.

- Evaluate the impact of inflation and the Russia/Ukraine, Israel/Hamas, and Iran/Israel conflicts on logistics costs and capacity constraints. Ensure that key trading partners are not on sanctions lists.

Near-term:

- For companies that have cargo moving through the Suez Canal and the Strait of Hormuz, evaluate the impact of extended rerouting.

Long-term:

- Evaluate supplier and factory location density to mitigate reliance on over-taxed trade lanes and regions of the globe currently experiencing geopolitical conflict or that have the potential for conflict. Density creates economy of scale but also risk, and subsequent logistics capacity crisis highlights the downside.

Notes:

- This report uses the initial compiled release of publicly available U.S. Customs and Border Protection (CBP) Bill of Lading (BOL) data for all U.S. ports, which provides a standard, official source of data for reporting on maritime trade. This data can be subject to modification later by CBP. The modified data can be seen in Descartes Datamyne™ where U.S. maritime records are processed daily. Descartes Datamyne is ISO 9001 certified.

- In Descartes Datamyne™, twenty-foot equivalent units (TEU) are calculated using a combination of container size and weight as declared on Bills of Lading filed with U.S. Customs and Border Protection (CBP).

Subscribe to the Global Shipping Report

Stay informed with the latest shipping trends and U.S. container import logistics data every month with the Descartes Global Shipping Report

About Descartes Datamyne

Leverage the Power of Global Import and Export Trade Data

Optimize trade lanes, expand into new markets, discover alternative buyers and suppliers, as well as spot supply and demand shifts from a single integrated web-based platform to cost-effectively enhance your supply chain resilience and competitive edge.

Special Reports

2024 Top 30 U.S. Port Report

Stay informed with the annual U.S. Port Report from Descartes, ranking 2024 Maritime Port performance and trends in a year that defied expectations.

Download the 2024 Top 30 U.S. Port Report

What Companies are Doing to Tackle Escalating Global Supply Chain Challenges

Offering must-read insights for global trade, this white paper provides an overview of the key challenges facing global supply chain leaders as discovered through Descartes’ 2024 Global Trade Intelligence Survey.

Download the White Paper

How Descartes Can Help

Descartes Datamyne delivers business intelligence with comprehensive, accurate, up-to-date, import and export information.

Our multinational trade data assets can be used to trace global supply chains and our bill-of-lading trade data – with cross-references to company profiles and customs information – can help businesses identify and qualify new sources. Ask us for a free, no obligation demonstration of our data on a product or trade commodity of your choosing – and keep the custom research we create with our compliments.