The last year of hyper-inflated business, capacity shortage, workforce constraints and increasing customer service demands have pushed leading forwarders to adopt digitization as a key strategy for thriving in the future. Digitization is the combination of business transformation with enabling technology to measurably impact competitive and company performance. According to the 7th Annual Forwarder & Broker Benchmark Study, adoption of digitization strategies and related technology investments have become the #1 priority for forwarders (and more so for the top performing ones) for the next 2 years. Here are the report findings that explain why this is happening and where investments in digitization are being made.

Why is digitization so important? Top responses included competitive pressure, addressing industry and regulatory change, and improving margins.

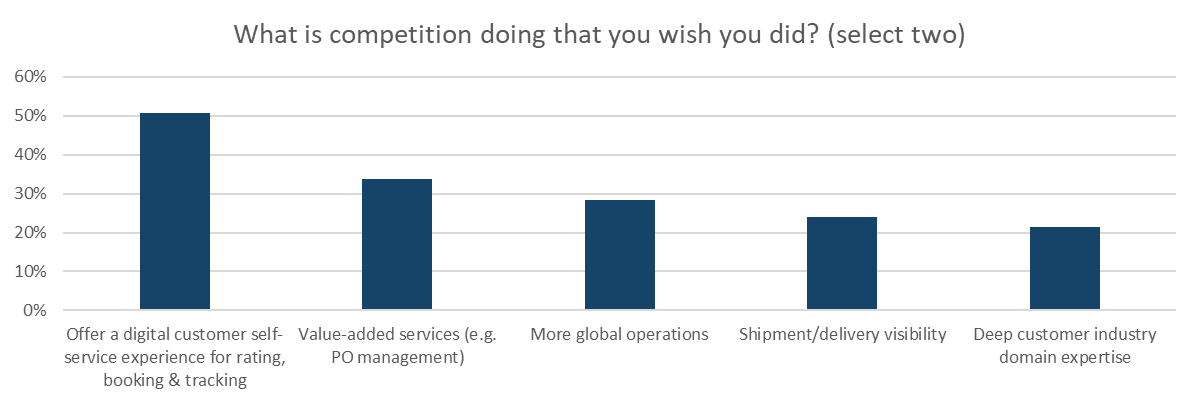

Competition. Competitive pressure is a key driver of change in any organization as they are pushing their digital prowess. The top cited competitor capability in the 2022 benchmark was to offer a digital customer self-service experience at 50% (see Figure #1), up 11% from 2021. Value-added services – which typically combine digitization techniques with new operational capabilities, was the second highest response at 34% and up 7% from 2021.

Figure #1: Competition and Digitization

Change. The global logistics community is undergoing trendemous change driven by economic and industry factors and forwarders and brokers are turing to technology to address them. Digitization requires technology and investing in technology was the top choice to address change at 77% - up 10% versus the 2021 benchmark. Top Performers – those companies with the best financial margins, are even more focused on investing in technology at 85% than Bottom Performers – those companies with the worst financial margins, at 61% (See Figure 2).

Figure 2: Preparing for Change

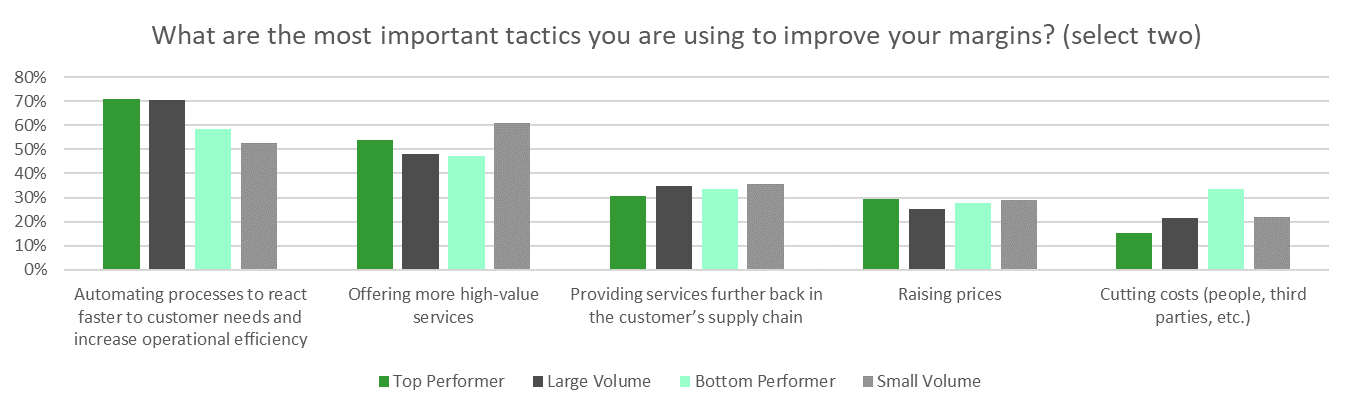

Margins. Financial margins have always been a challenge for forwarders and brokers. To improve margins, respondents selected automating processes in 2022 as the top overall response at 61% and an increase of 14% over 2021. Offering more high value services was a close second at 59% and also an indicator of digitization as many of them are technology enabled. However, the approach to addressing change varied by financial performance with Top Performers more focused on value creation (automation agility, high value services and services extension) than Bottom Performers in the 2022 benchmark (See Figure 3). Bottom Performers are greater than two times more focused on cutting costs to improve margins than Top Performers (33% versus 15%, respectively).

Figure 3: Tactics to Improve Margins

Where are forwarders and brokers going to focus their IT efforts and investment? Digitization again rises to to the top with Top Performers even more committed to their digital agenda. There is tight alignment with forwarders and brokers on where they believe the greatest IT value is and the investments they intend to make for the next two years.

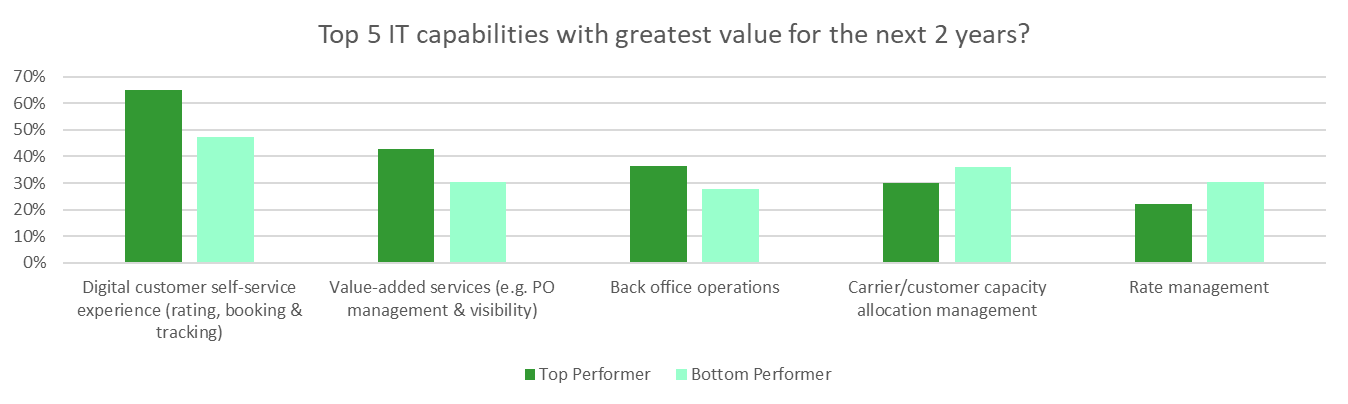

Value. Customer-facing systems dominated forwarder and broker thinking for the greatest IT value for the next 2 years, where the top overall response was digitization of customer self-service at 59% - an increase of 6% over 2021. Top Performers were much more focused on digitization (digital customer experience, value-added services and back office operations) than Bottom Performers (See Figure 4). Value added services (36%) and back office operations (34%) – 2 other areas impacted by digitization were the second and third responses, respectively. New choice for 2022 - carrier/customer capacity allocation management came in very close at #4 overall (33%) followed by another new choice, rate management, at #5 (26%).

Figure 4: IT Capability with Greatest Future Value

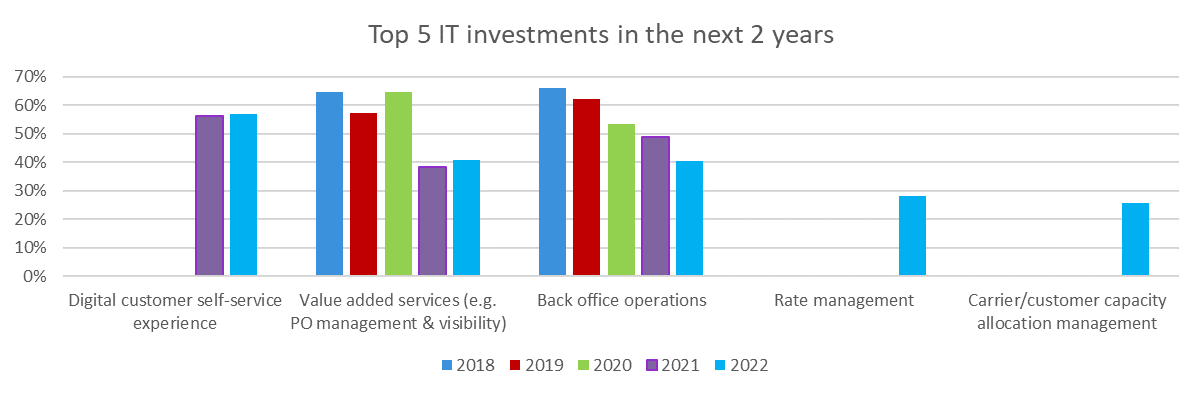

Investment. There was little divergence from IT value to IT investment in the 2022 benchmark. This cannot be understated as forwarders and brokers are allocating strategic investment directly in line with areas of most value. Digital customer self-service was the top overall investment (57%) in the 2022 benchmark, a repeat of 2021. New choices rate management (28%) and carrier/customer capacity allocation management (24%) came in at #4 and #5, respectively – a minor flip in priority from perceived IT value. Again, Top Performers are more focused on digitization (digital customer experience, value-added services and back office operations) investments than Bottom Performers.

The global logistics industry is undergoing tremendous change because of the increased demand for shipping and the challenges associated with carrier capacity and workforce shortages. Instead of trying to just be better, forwarders and brokers are turning to digitization to transform their operations and customer experience. Top Performers are leading the way in digitization by being more focused on value creation and the IT investment that supports it. What is your organization’s digitization strategy and how much investment is it making to make a difference? Let me know.