ATLANTA, Georgia, March 10, 2026 -- Descartes Systems Group, the global leader in uniting logistics-intensive businesses in commerce, released its March Global Shipping Report for logistics and supply chain professionals. In February 2026, U.S. container import volumes were 2,093,422 twenty-foot equivalent units (TEUs), down 9.7% month-over-month, reflecting typical seasonal patterns. China-origin imports decreased 5.5% month-over-month after posting a 9.3% increase in January. Port transit delays showed mixed but moderate changes in February, with no signs of widespread congestion. With military conflict in the Middle East, changes to U.S. tariffs, continued transatlantic trade friction and revised U.S.–India tariff terms, the February update of the logistics metrics monitored by Descartes suggests supply chain planning remains centered on risk management and flexibility as trade conditions are increasingly shaped by geopolitical escalation and policy shifts.

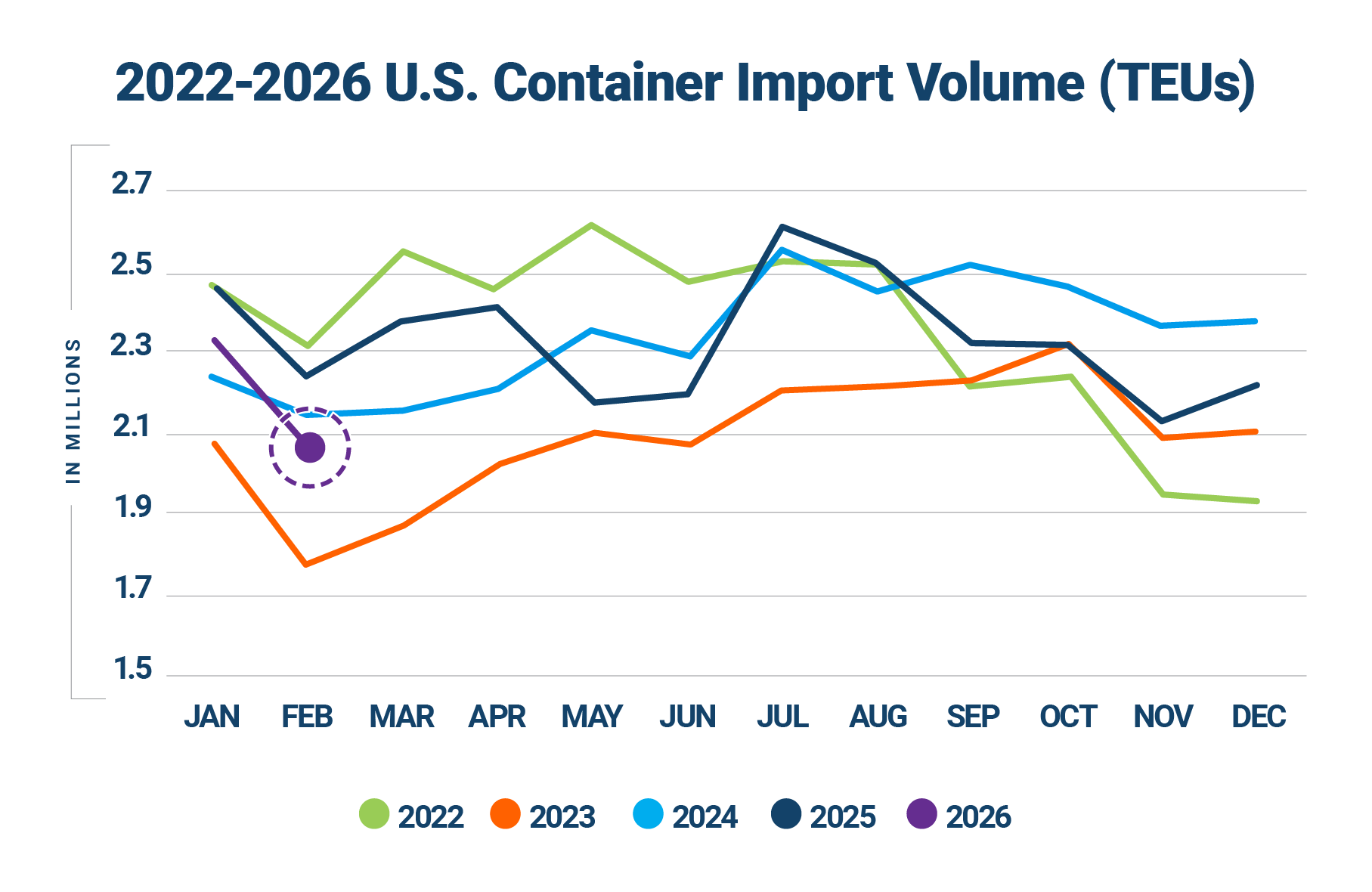

February U.S. container imports decline month-over-month but remain seasonally resilient.

While imports were down 9.7% from January and 6.5% compared to February 2025 (see Figure 1), volumes were typical of February levels observed post-pandemic and remained 17.0% above February 2019. Despite the pullback, February 2026 ranks as the fourth-strongest February on record. Unlike February 2025, when frontloading likely inflated volumes, February 2026 activity suggests a normalized trade environment, with importers operating within ongoing policy uncertainty rather than accelerating shipments in anticipation of it.

Figure 1. U.S. Container Import Volume Year-over-Year Comparison

Source: Descartes Datamyne™

Top countries of origin (CoO) volumes decline in February, with broad-based decreases across Asia.

In February 2026, U.S. containerized imports from the top 10 CoO fell 9.4% month-over-month, with widespread losses across major sourcing countries (see Figure 2). After posting a 9.3% month-over-month increase in January, China recorded the largest volume decrease in February, down 5.5% (42,531 TEUs), with declines observed across most major product categories. Other decreases included Vietnam at 11.6% (33,542 TEUs), Thailand at 19.9% (24,038 TEUs), India at 17.5% (18,093 TEUs) and South Korea at 17.0% (15,261 TEUs). Only two countries posted gains: Germany increased 5.5% (2,510 TEUs) and Hong Kong edged up 0.4% (303 TEUs). Overall, February results reflect broad-based softness across leading Asian markets, contributing to the overall pullback in U.S. volumes.

Figure 2. January 2026 to February 2026 Comparison of U.S. Import Volumes from Top 10 Countries of Origin

Source: Descartes Datamyne™

“While February volumes suggest underlying demand remains relatively stable, the military conflict in the Middle East, evolving U.S. tariffs and ongoing trade tensions have increased routing, cost and policy uncertainty for importers,” said Jackson Wood, Director of Industry Strategy at Descartes. “To minimize global shipping challenges, importers remain focused on strategies, tactics and technologies to help navigate disruption, manage cost exposure, and strengthen supply chain resilience in a global trade environment characterized by ongoing volatility.”

Descartes began its global shipping analysis in August 2021. To read past monthly reports, learn more about the key economic and logistics factors driving global shipping, and review strategies to help address challenges in the near-, short-, and long-term, visit Descartes’ Global Shipping Resource Center.

About Descartes

Descartes powers more responsive, efficient, secure and sustainable international and domestic supply chains by uniting logistics-intensive businesses on its Global Logistics Network (GLN). Shippers, carriers, and logistics service providers connect and collaborate on the GLN leveraging technology, data and AI to manage last mile deliveries, domestic and international shipments, transportation rating and payment, global trade research, customs compliance and a variety of regulatory processes. Learn more about Descartes (Nasdaq:DSGX) (TSX:DSG) at www.descartes.com and connect with us on LinkedIn and X.

Global Media Contact

Cara Strohack

Tel: 226-750-8050

cstrohack@descartes.com

Cautionary Statement Regarding Forward-Looking Statements

This release contains forward-looking information within the meaning of applicable securities laws (“forward-looking statements”) that relate to Descartes’ global trade intelligence solution offerings and potential benefits derived therefrom; and other matters. Such forward-looking statements involve known and unknown risks, uncertainties, assumptions and other factors that may cause the actual results, performance or achievements to differ materially from the anticipated results, performance or achievements or developments expressed or implied by such forward-looking statements. Such factors include, but are not limited to, the factors and assumptions discussed in the section entitled, “Certain Factors That May Affect Future Results” in documents filed with the Securities and Exchange Commission, the Ontario Securities Commission and other securities regulatory authorities across Canada including Descartes’ most recently filed annual and interim management’s discussion and analysis which are available under Descartes’ profile through the EDGAR website at http://www.sec.gov or through the SEDAR+ website at http://www.sedarplus.com/. If any such risks actually occur, they could, among other consequences, materially adversely affect our business, financial condition or results of operations. In that case, the trading price of our common shares could decline, perhaps materially. Readers are cautioned not to place undue reliance upon any such forward-looking statements, which speak only as of the date made. Forward-looking statements are provided for the purposes of providing information about management’s current expectations and plans relating to the future. Readers are cautioned that such information may not be appropriate for other purposes. We do not undertake or accept any obligation or undertaking to release publicly any updates or revisions to any forward-looking statements to reflect any change in our expectations or any change in events, conditions or circumstances on which any such statement is based, except as required by law.