The below information has been collected regarding the Union Custom Code (UCC) updates within in the EU.

We encourage you to bookmark this page and check back often for up-to-date information. On this page you will find general information about the UCC. Also available is country specific FAQs for UK and the Netherlands/Belgium.

Union Customs Code - Frequently Asked Questions (FAQs)

What is the Union Customs Code (UCC)?

The UCC is an update to customs legislation across the EU, and will introduce a number of revisions to existing requirements. The UCC was formalised with Regulation (EU) No 952/2013, and applies beginning 1 May 2016 when associated Delegated and Implementing Acts came into force.

A number of transitional phases are following until full implementation in 2020. These measures are captured in the Transitional Delegated Act (TDA). The main reason for the transitional measures is that the IT systems that need to support the UCC are not complete.

Why was the UCC created?

The UCC was enacted in order to modernise and simplify trade into and within the EU. It also aims for a harmonisation of customs procedures across the member states. Some additional goals of the regulation are to increase the safety and security of goods as well as to streamline processes. The key principle of the UCC is that all customs declarations should be electronic.

Who will be affected by the UCC?

Business involved in the import and/or export of goods into and within the EU will be affected. This includes warehouse operators, third-party logistics service providers (3PLs), freight forwarders, customs brokers, shippers, agents, intermediaries and others. There is impact on following domains:

- Changes to customs procedures and authorisations - Some examples include the end of Inward Processing Relief (IPR) drawback and customs warehouse type D, as well as the end of the first point-of-sale (although some exceptions still exist)

- Modifications to existing electronic procedures

- Introduction of new digital processes, including the Proof of Union Status

Will there still be differences between the EU member states?

Yes. The EU creates the Implementing and Delegated Acts, which have to be translated in the legislation of the member states. This may lead to different interpretations. The impact is also not the same for all countries, as it depends to what extent specific procedures are already aligned with the UCC, and whether the country decided to make changes in an existing system or create a completely new solution.

What is the roadmap for the IT systems?

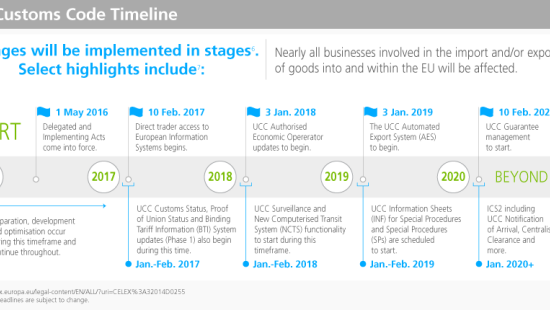

Currently there are no detailed technical specifications yet of the changes. The IT system changes are incorporated in the Multi-Annual Strategic Plan (MASP), which is revised frequently to adjust the timings and projects. Below is an overview of the most relevant IT projects in the MASP in relation to the UCC, with the latest update as of November 2015:

The above timeline includes select highlights of the UCC implementation programme and can be summarized as follows for reference:

- 2016 – on: Preparation, development and optimization occur during this timeframe and continue throughout

- 10 Feb 2017: Direct trade access to European Information Systems beings.

- Jan. - Feb. 2017: UCC Customs Status, Proof of Union status and Binding Tariff Information (BTI) System updates (Phase 1) begin during this time.

- 3 Jan. 2018: UCC Authorised Economic Operator updates to begin.

- Jan. – Feb. 2018: UCC Surveillance and New Computerised Transit System (NCTS) functionality to start during this timeframe.

- 3 Jan. 2019: The UCC Automated Export System (AES) to begin.

- Jan. – Feb. 2019: UCC Information Sheets (INF) for Special Procedures and Special Procedures (SPs) are scheduled to start.

- 10 Feb. 20202: UCC Guarantee management to start.

- Jan 2020+: ICS2 including Notification of Arrival, Centralized Clearance and more.

What is the UCC Timeline

As per the above, for many projects, the timing is not fixed and will be implemented in stages. The above matrix must be mapped to the different countries as an extra dimension. This is especially the case for items that do not depend on central components. In addition, countries can decide to start earlier than the go-live date planned by EU, which can be challenging for companies that have business in multiple countries.

Not all of the above projects have a direct impact on the electronic declaration systems. There are also projects for central European databases, for example for authorization; or electronic systems to apply for a Binding Tariff Information (BTI) or a license.

Does the UCC bring changes to safety and security?

Yes. One of the changes is the introduction of multiple filing, to obtain more detailed information for risk analysis. Currently, carriers file the Entry Summary Declaration (ENS), which is a pre-arrival declaration for risk analysis. The current system is called Import Control System (ICS), which will be upgraded to ICS2. The impact is that in addition to the carrier, the freight forwarder or even the consignee will need to supply information.

The detailed specifications will be defined in 2017 and 2018, and the go-live is planned by the end of 2020. On the technical side, the plan is to create a central European repository to collect all the data. The requirement to file the ENS will also be extended to postal and express service providers.

Is there new or revised terminology associated with the UCC?

Yes. The UCC introduces several updated terms for use in customs language including:

| Before | After |

|---|---|

| Community goods | Union goods |

Customs Procedures with Economic Impact (CPEI) |

Special Procedures |

| Local Clearance Procedure (LCP) | Entry in the Declarant’s Records |

| Community Transit | Union Transit |

| New Computerised Transit System (NCTS) | Electronic Transit System (ETS) |

Will the UCC require companies to be more compliant?

Yes, there will be more checks on the correct application of authorisation, for example. To get more benefits, it will be important to show a solid record of compliance, and in most cases, it requires an Authorised Economic Operator (AEO) certificate.

How does the UCC impact Authorised Economic Operators (AEOs)?

One of the more important provisions of the UCC is the increased prominence of the AEO. The UCC includes a number of benefits for businesses with AEO status or that meet AEO status criteria. These include reduced guarantees and easier access to customs simplifications which could result in a competitive advantage.

Will the UCC increase AEO application levels?

It is anticipated that the new legislation will boost interest in and applications for AEO status. This may especially be the case for businesses that use customs procedures such as Inward Processing, Customs Warehousing and others when new guarantees are required under the UCC (see below).

What are the qualifications to become an AEO?

To become an AEO, a trader must have a solid record of compliance, a satisfactory system to manage both commercial and transport-related data, adequate record-keeping capabilities, proven business solvency and maintain high safety standards. An AEO trader should also ensure that they have technology in place that is capable of facilitating audit-based controls and that can properly identify customs statuses. Under the UCC, they should also be able to show they have practical standards of competence or professional qualifications relating to the customs activities which they carry out.

What are the UCC declaration types?

The UCC declaration types are:

- Full

- Simplified Declaration Procedure (SDP)

- Entry in the Declarant’s Records (EIDR)

In the UK, for example, both EIDR and SDP can relieve the need to submit a supplementary declaration when used to enter the goods into Customs Warehousing. An EIDR is similar to the previous Local Clearance Procedure (LCP). Unless waived, only an electronic notification will be required at the time of release rather than a customs declaration.

Please note that an EIDR cannot be used to enter goods for:

- Temporary Storage (TS)

- Onward Supply Relief (OSR)

- Transit

- Special procedures where an Information Sheet Form (INF) is required

- On export where a pre-departure declaration is required

The UCC also sets the legislative framework for:

- Centralised Clearance, where a trader can deal with a single Customs Authority whilst importing and exporting via multiple Member States, and

- Self-Assessment, where a company can manage their customs activities through their own systems to determine their duty liability which will be periodically notified to customs

What is a UCC guarantee?

Under the UCC, any known or potential customs debts must be secured by a guarantee. More specifically, in order to ensure the receipt of duties and taxes, a guarantee or insurance of duty payment is now required across all Member States. This includes not only known debts deferred for later payment, but any duties suspended and is extended to the first time for those traders operating Inward Processing, End use, Temporary Storage facilities and Customs Warehousing.

Companies with an AEO status, or that meet the certain criteria required to be an AEO, will be eligible to apply for a guarantee reduction or waiver under certain conditions.

Under the transitional arrangements, although mandatory guarantees were introduced on 1 May 2016, they will not apply until a company’s special procedure authorisation has been reassessed or reissued as a UCC authorisation.

How will the guarantee amount be determined?

The guarantee amount will vary by country and circumstance. In the UK for example, HM Revenue & Customs (HMRC) will review a company to determine the guarantee figure. If adequate information is not available, a guarantee of €10,000 will be required per declaration. Comprehensive guarantees are also available to cover more than one transaction. In order to secure a comprehensive guarantee, a trader must:

- Be established in the customs territory of the Union

- Satisfy all of the prerequisite AEO requirements

In addition, a business must also meet one of the following criteria:

- Regularly use customs procedures

- Operate a Temporary Storage (TS) facility

- Fulfil AEO competence or professional qualification standards

The UCC and technology

The UCC requires that all exchange of information between customs authorities and companies must be electronic. This includes customs declarations, applications as well as notifications. Companies may secure a reduced guarantee if advanced technology in place that maintains sufficient audit controls as part of their meeting AEO criteria or holding AEO status. The UCC also recognises the growth of internet sales and allows for remote retail sale of goods whilst in a customs warehouse. This covers goods sold via the internet or any other distance-selling method.

The UCC and Descartes

Descartes is a leading logistics technology provider that offers solutions to fully manage customs declarations and fiscal compliance processes. Our solutions can help traders, brokers and forwarders keep pace with changing regulations such as the UCC and others to achieve a potential competitive advantage.

Descartes is active in about 15 European countries for Customs declarations, duty management and related functionalities. Through our membership of EurTradeNet, several national customs software associations and more, Descartes keeps up-to-date on the latest developments. Descartes is currently already offering the ICS solution in all EU member states, which will also support ICS2 and the multiple filing.

Click here to ask us how we can help you and for more information.

Additional Resources