The Global Shipping Report

June U.S. Containerized Imports Remain Stable Amid Global Trade Tensions

Stay informed with the latest insights from the Descartes Global Shipping Report

Data for the Global Shipping Report provided by Descartes Datamyne

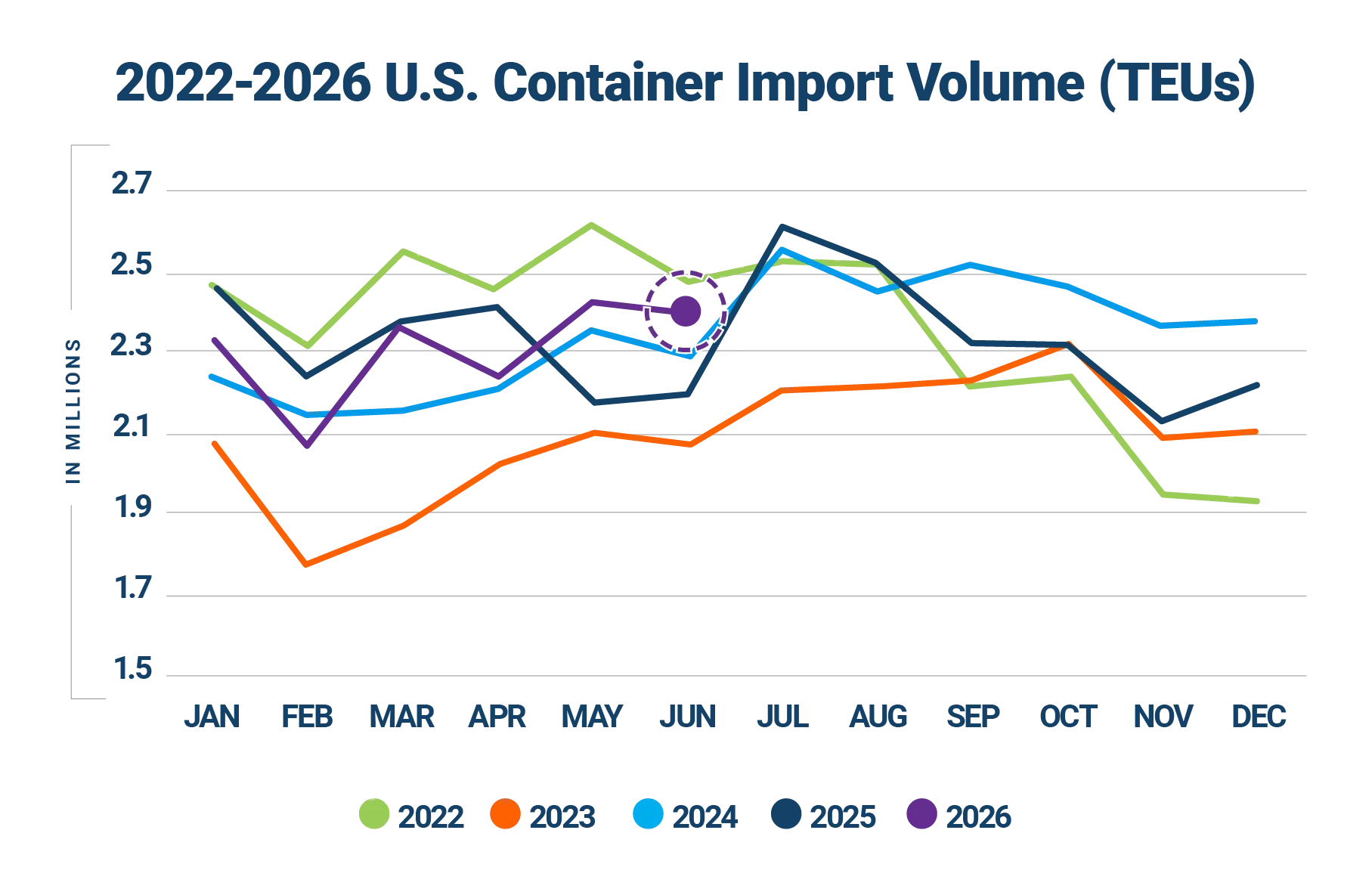

U.S. containerized imports remained stable in June 2026, totaling 2,400,627 twenty-foot equivalent units (TEUs). Volumes declined 1.2% from May, reflecting the typical seasonal easing that follows May’s import growth, but were still 8.2% higher than June 2025. Through the first half of 2026, imports were nearly flat year-over-year, down just 0.3%.

China-origin imports held steady following May’s rebound, totaling 814,474 TEUs in June. Volumes dipped just 0.2% month-over-month and increased 27.4% year-over-year. Imports from the top 10 countries of origin were also largely stable, declining only 0.3% from May while rising 13.2% from June 2025. China accounted for most of the year-over-year growth, underscoring its continued influence on U.S. import volumes even as sourcing diversification remains a priority for importers.

Port activity was mixed. Los Angeles posted a strong volume increase that helped lift West Coast share, while several East and Gulf gateways recorded declines. Gulf Coast imports pulled back sharply after May’s surge, and port transit delays improved across most East and Gulf Coast ports even as Los Angeles delays rose.

The broader trade environment remains unsettled. Strait of Hormuz risks, evolving U.S. tariff policy, lower Panama Canal draft limits, and persistent Red Sea disruptions continue to shape freight costs, routing decisions, and sourcing strategies. For importers, June results point to a market balancing steady import volumes against elevated geopolitical and policy uncertainty.

In this Article...

- U.S. container imports reached 2,400,627 TEUs in June 2026.

- June 2026 imports decreased by 1.2% over May and were 8.2% higher than June 2025.

- June 2026 imports from China were 814,474 TEUs, down 0.2% from May and up 27.4% from June 2025.

- June 2026 U.S. imports from the top 10 countries of origin (CoO) decreased by 0.3% over May and were up 13.2% over June 2025.

- Top 10 ports captured 84.3% of total imports in June.

- East and Gulf Coast port delays improved, while Los Angeles delays nearly doubled.

- Gulf Coast imports decreased by 17.3% in June and were 5.1% below the 12-month rolling average.

- Strait of Hormuz disruptions continue to threaten global shipping.

- Evolving U.S. tariff policies continue to add uncertainty to global trade.

- Lower Panama Canal draft limits add another layer of supply chain uncertainty.

- Red Sea disruptions continue to pressure global shipping capacity and freight rates.

- Key points to monitor and manage supply chain risks.

- Recommendations to help mitigate global shipping challenges.

June U.S. container imports ease slightly from May.

U.S. containerized imports reached 2,400,627 TEUs in June 2026, dipping 1.2% from May but remaining 8.2% above June 2025 levels, suggesting import demand remains resilient despite ongoing trade and tariff uncertainty (see Figure 1). For the first six months of the year, volumes were down slightly by 0.3% but remained 22.2% above the same period in pre-pandemic 2019.

Figure 1: U.S. Container Import Volume Year-over-Year Comparison

Source: Descartes Datamyne™

Over the last 10 years, June import volumes have trailed May levels, with the exception of 2020 and 2025 (see Figure 2). The month-over-month decline follows the seasonal month-over-month increase typically observed from April to May.

Figure 2: May to June U.S. Container Import Volume Comparison

Source: Descartes Datamyne™

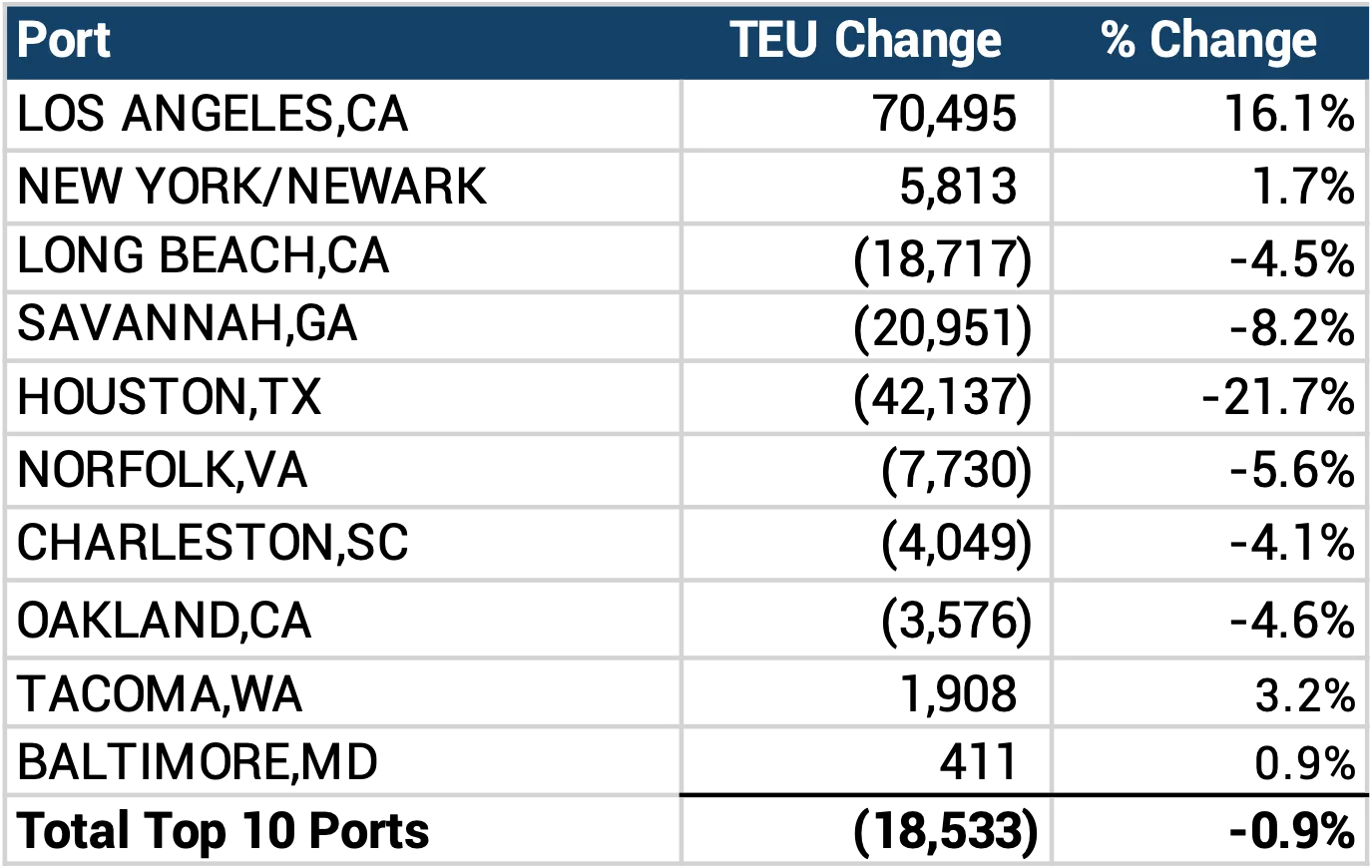

June import volumes were mixed across major U.S. gateways.

Container volumes across the top 10 U.S. ports declined by 18,533 TEUs in June 2026, a 0.9% month-over-month decrease, with six of the ten major gateways posting lower volumes compared to May (see Figure 3). Los Angeles recorded the largest volume increase, rising 16.1% (70,495 TEUs), followed by New York/Newark, up 1.7% (5,813 TEUs). Smaller gains were reported at Tacoma, up 3.2% (1,908 TEUs), and Baltimore, up 0.9% (411 TEUs).

In contrast, Houston posted the steepest decline, falling 21.7% (42,137 TEUs), followed by Savannah, down 8.2% (20,951 TEUs), and Long Beach, down 4.5% (18,717 TEUs). Other declines were reported at Norfolk (5.6%), Oakland (4.6%), and Charleston (4.1%). The mixed results suggest that June’s slight pullback in import activity was not evenly distributed, with gains at Los Angeles and New York/Newark helping to offset sharper declines at several Gulf Coast and West Coast gateways.

Figure 3: May 2026 to June 2026 Comparison of Import Volumes at Top 10 U.S. Ports

Source: Descartes Datamyne™

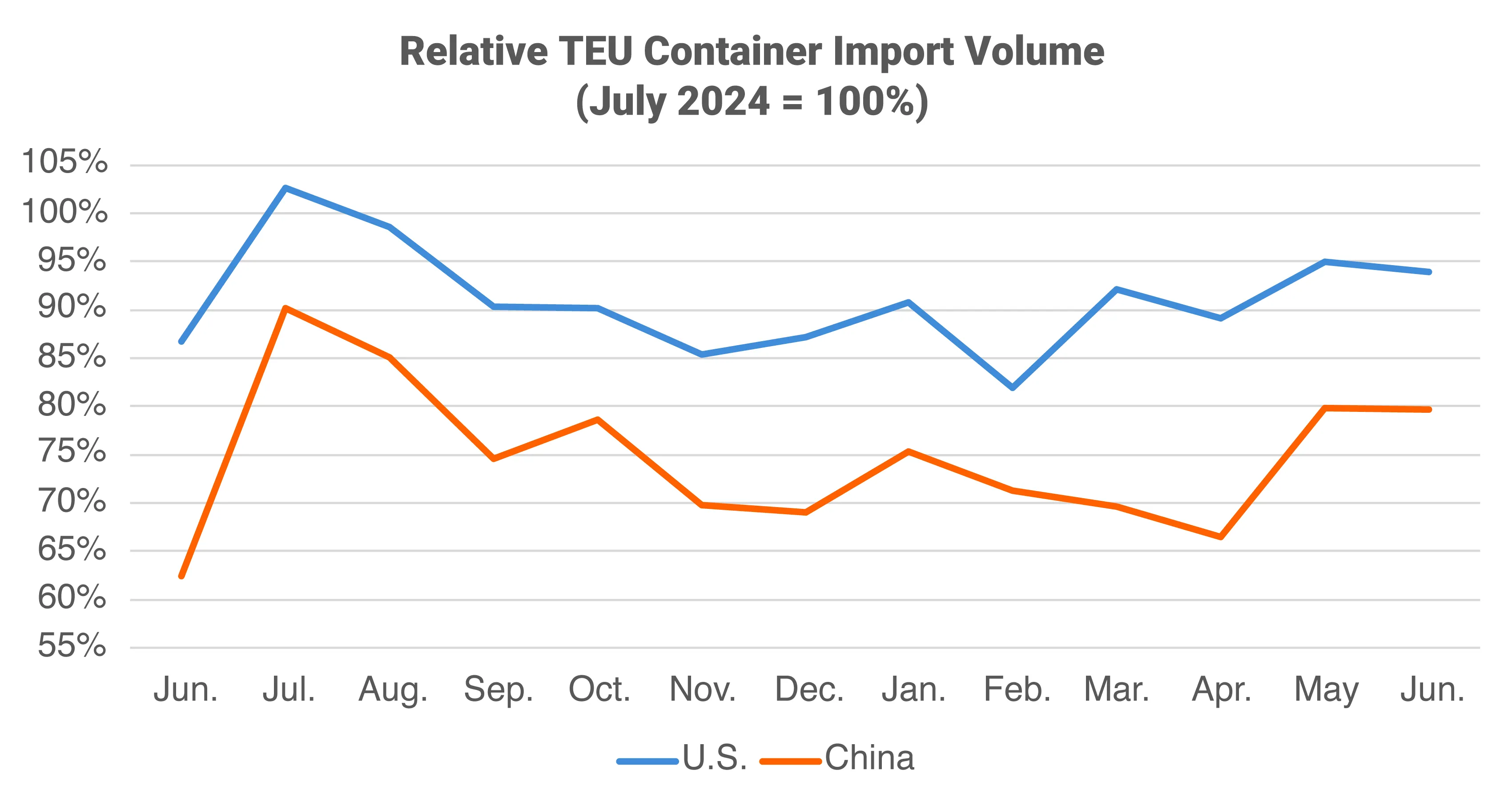

China-origin imports hold steady in June.

U.S. containerized imports from China totaled 814,474 TEUs in June 2026. Following May’s sharp rebound, volumes were essentially flat, declining just 0.2% month-over-month while increasing 27.4% compared to June 2025 (see Figure 4). China’s share of total U.S. containerized imports rose to 33.9%, up slightly from May’s 33.6% and well above June 2025’s 28.8%. Despite the year-over-year gain, June volumes remained 20.4% below the July 2024 peak of 1,022,913 TEUs, indicating that imports from China remain below recent highs as importers continue to adjust sourcing strategies amid ongoing trade tensions.

China’s import mix remained was led by plastics (HS-39) and furniture and bedding (HS-94), which accounted for 15.7% and 14.7% of June volume, respectively. Machinery (HS-84) and electrical machinery (HS-85) represented a combined 17.7% of imports, highlighting the continued importance of industrial goods. Consumer-oriented categories also remained significant, with toys and sporting goods (HS-95) accounting for 7.4% of volume, while apparel, textiles, and footwear categories collectively contributed 9.3%. Overall, June China-origin imports were supported by broad-based year-over-year gains across both consumer and industrial segments.

Figure 4: June 2025–June 2026 Comparison of U.S. Total and Chinese TEU Container Volume Relative to Chinese Import Record

Source: Descartes Datamyne

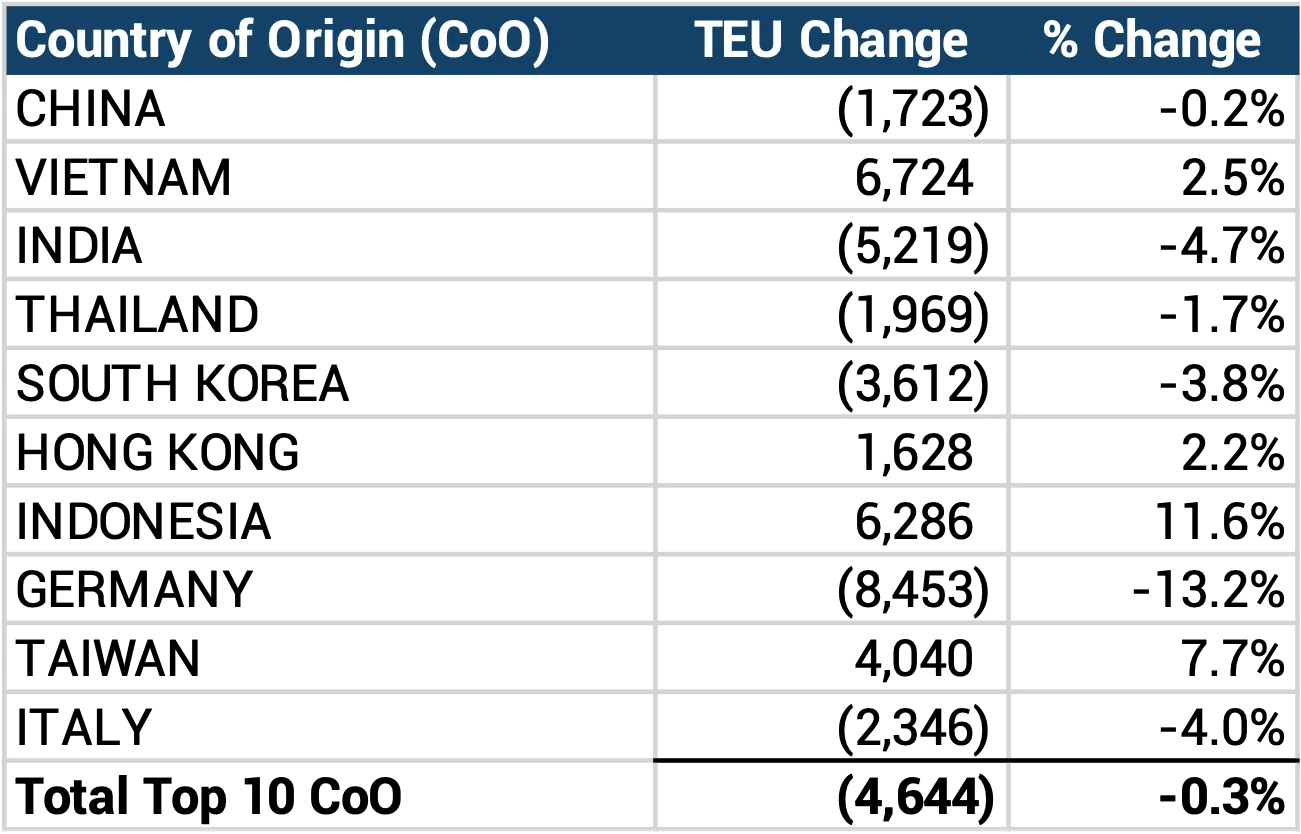

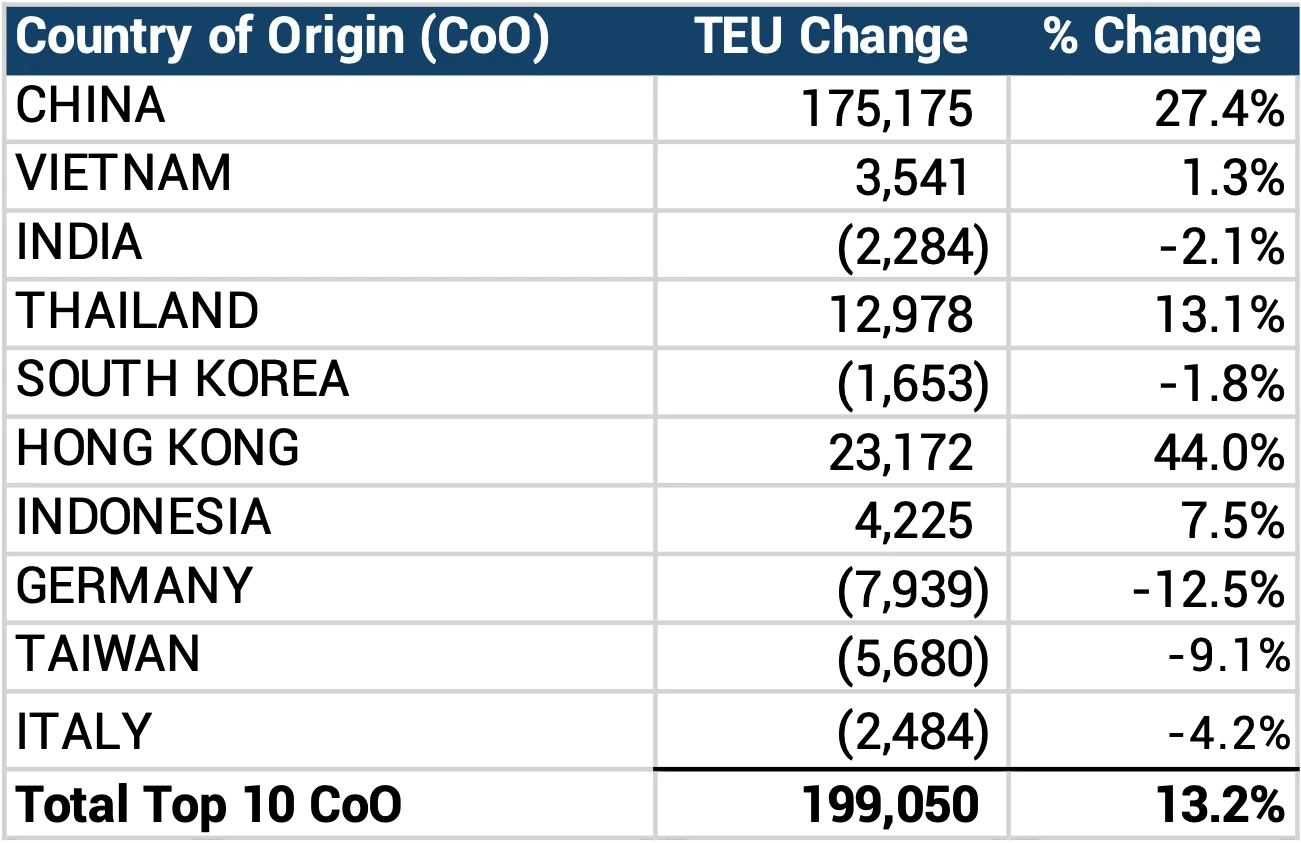

China drives year-over-year gains among top 10 CoO.

In June 2026, U.S. containerized imports from the top 10 CoO increased 13.2% year-over-year, representing a combined gain of 199,050 TEUs (see Figure 6). The growth was driven primarily by China, where volumes rose 27.4% (175,175 TEUs), along with gains from Hong Kong (44.0%), Thailand (13.1%), Indonesia (7.5%), and Vietnam (1.3%). Offsetting some of the growth, declines were recorded for Germany (12.5%), Taiwan (9.1%), Italy (4.2%), India (2.1%), and South Korea (1.8%). Overall, June results reflect strong year-over-year gains led by China, even as several major sourcing markets posted declines.

Figure 5: May 2026 to June 2026 Comparison of U.S. Import Volumes from Top 10 Countries of Origin

Source: Descartes Datamyne

China drives year-over-year gains among top 10 CoO.

In June 2026, U.S. containerized imports from the top 10 CoO increased 13.2% year-over-year, representing a combined gain of 199,050 TEUs (see Figure 6). The growth was driven primarily by China, where volumes rose 27.4% (175,175 TEUs), along with gains from Hong Kong (44.0%), Thailand (13.1%), Indonesia (7.5%), and Vietnam (1.3%). Offsetting some of the growth, declines were recorded for Germany (12.5%), Taiwan (9.1%), Italy (4.2%), India (2.1%), and South Korea (1.8%). Overall, June results reflect strong year-over-year gains led by China, even as several major sourcing markets posted declines.

Figure 6: June 2025 to June 2026 Comparison of U.S. Import Volumes from Top 10 Countries of Origin

Source: Descartes Datamyne

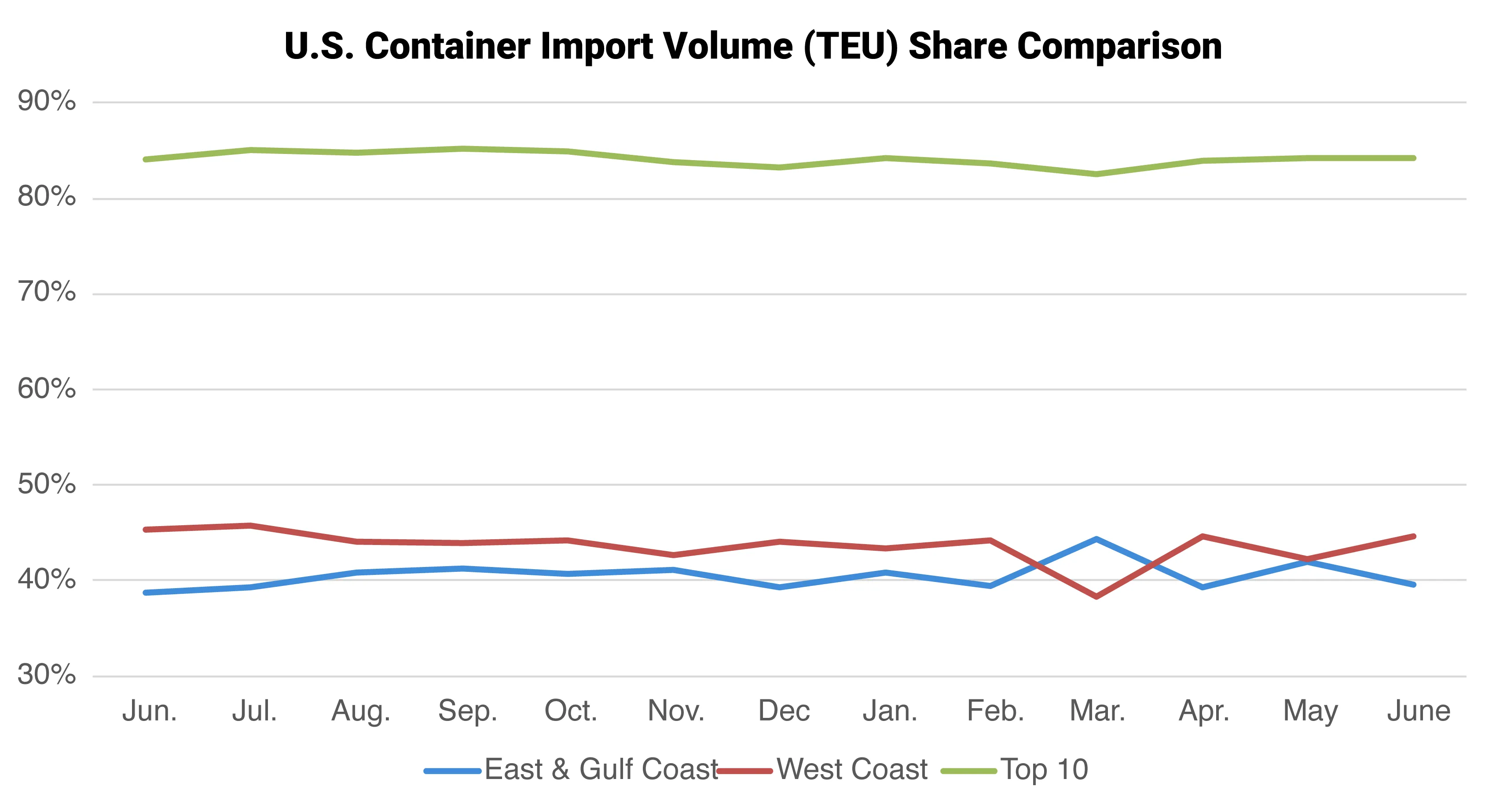

West Coast ports gain share as East and Gulf Coast share declines.

East and Gulf Coast ports accounted for 39.6% of total U.S. containerized imports, down from 42.0% in May, while West Coast ports increased their share to 44.6%, compared to 42.3% the previous month (see Figure 7). The top 10 U.S. ports handled 84.3% of total imports in June, unchanged from May. The results suggest that import volumes remained concentrated among the nation’s largest gateways, but with a shift toward West Coast ports as East and Gulf Coast gateways captured a smaller share of total activity.

Figure 7: Volume Analysis for Top Ports, West Coast Ports and East and Gulf Coast Ports

Source: Descartes Datamyne™

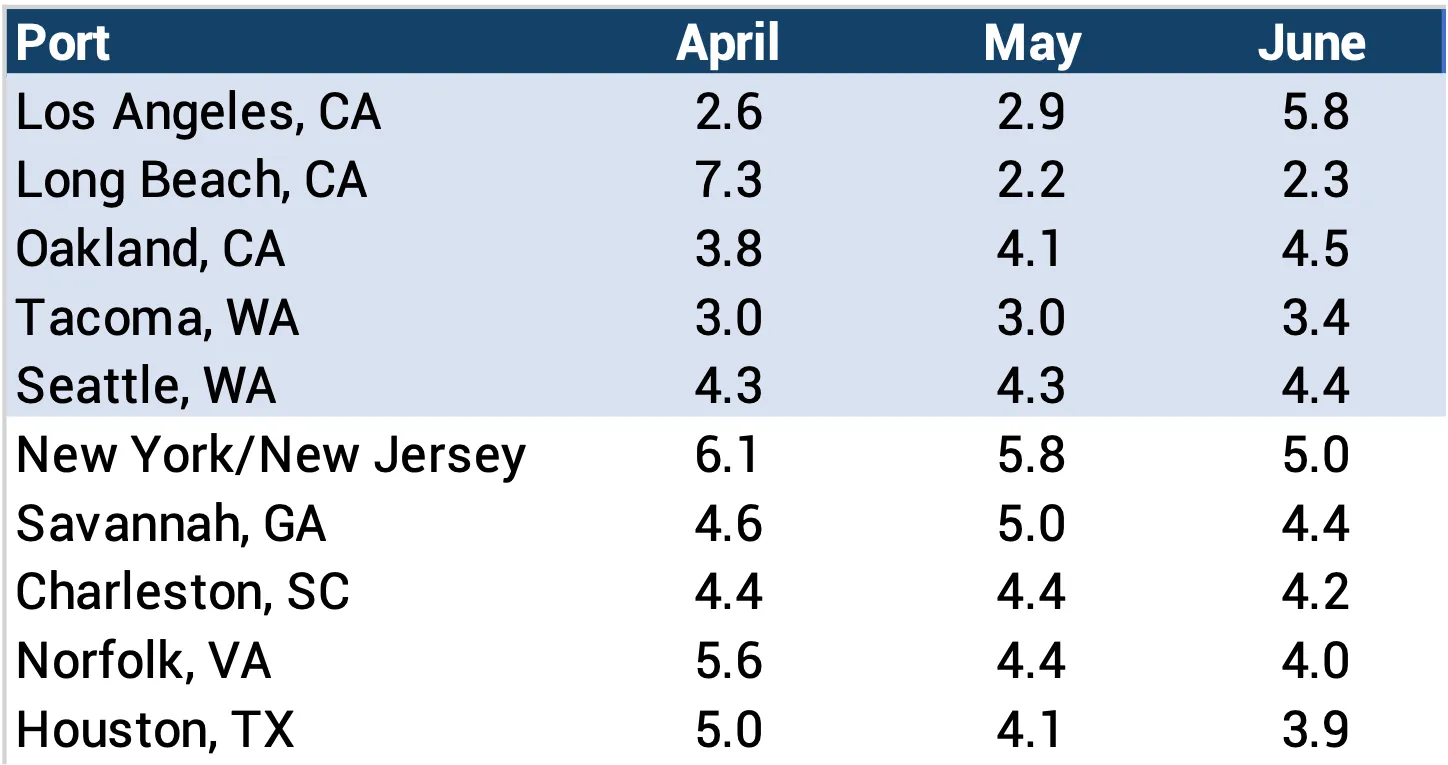

Port delays improve across East and Gulf Coast gateways as Los Angeles rises.

In June 2026, port transit delays were mixed across major U.S. gateways, with notable regional differences (see Figure 8). The most significant change occurred at Los Angeles, where delays increased from 2.9 days in May to 5.8 days in June, the highest delay among major gateways. On the West Coast, delays rose modestly at Oakland (0.4 days), Tacoma (0.4 days), Seattle (0.1 days), and Long Beach (0.1 days). Across the East and Gulf Coast, transit times improved broadly, including at New York/New Jersey (0.8 days), Savannah (0.6 days), Charleston (0.2 days), Norfolk (0.4 days), and Houston (0.4 days). Overall, June transit times suggest improving conditions across East and Gulf Coast gateways, while West Coast delays increased modestly, led by a sharper rise at Los Angeles.

Figure 8: Monthly Average Transit Delays (in days) for the Top 10 Ports (April – June 2026)

Source: Descartes Datamyne™

Note: Descartes’ definition of port transit delay is the difference as measured in days between the Estimated Arrival Date, which is initially declared on the bill of lading, and the date when Descartes receives the U.S. Customs and Border Protection (CBP) processed bill of lading data.

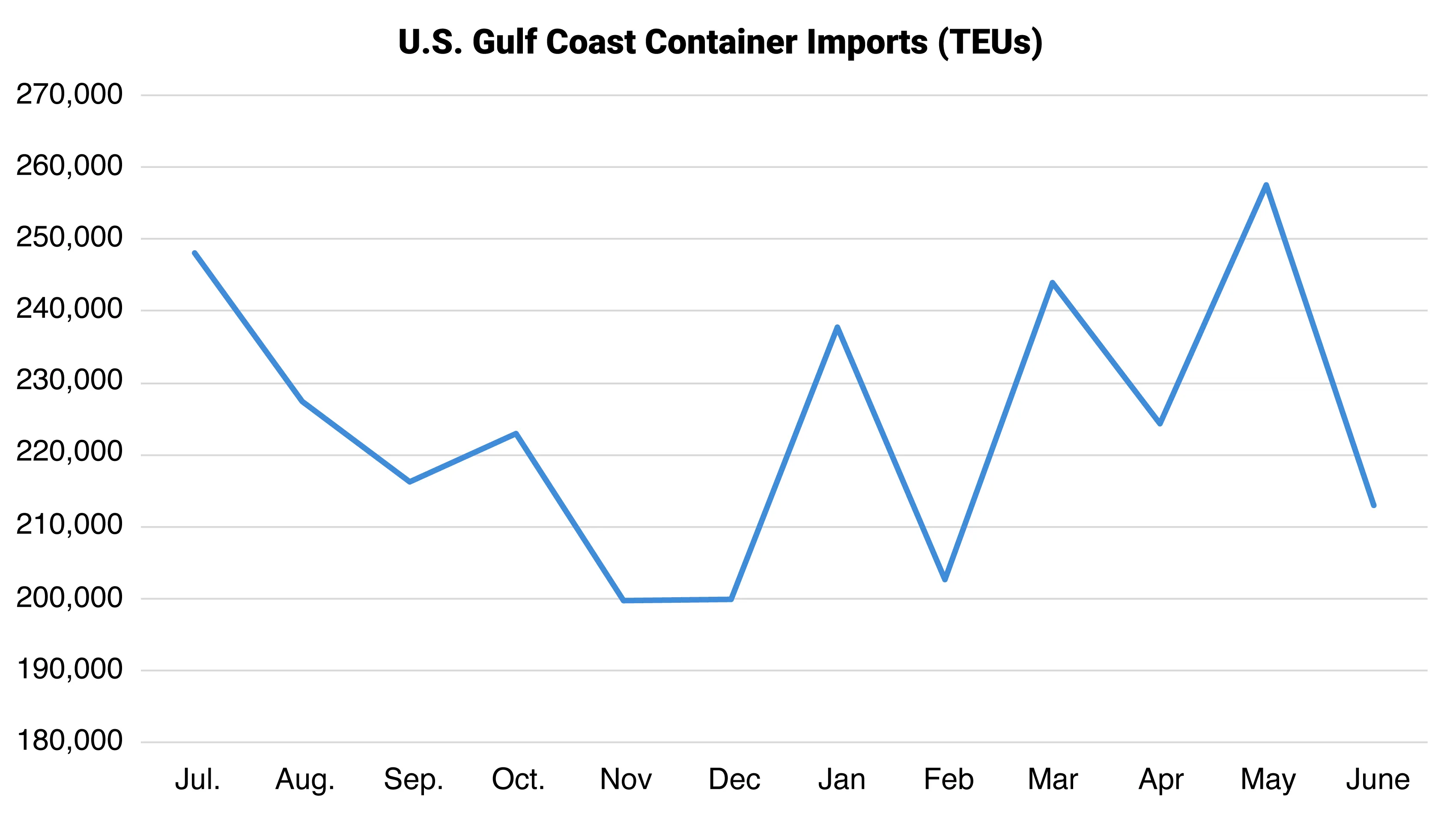

Gulf Coast imports decline after May surge.

Gulf Coast container imports pulled back in June 2026, totaling 213,075 TEUs, a 17.3% decrease from May (see Figure 9). The decline reversed much of May’s sharp gain (the second-highest monthly volume on record for the Gulf Coast) and brought volumes 5.1% below the rolling 12-month average of 224,470 TEUs. The results suggest May’s strength was not sustained into June, with Gulf Coast import activity cooling after a brief rebound.

Figure 9: May 2025 to June 2026 U.S. Gulf Coast Container Imports

Source: Descartes Datamyne™

Trusted by

Global Shipping Report Archive

Stay informed with monthly shipping insights with the Global Shipping Report

Director, Industry Strategy, Global Trade Intelligence, Descartes

Subscribe to the Global Shipping Report

Stay informed with the latest shipping trends and U.S. container import logistics data every month with the Descartes Global Shipping Report

About Descartes Datamyne

Leverage the Power of Global Import and Export Trade Data

Optimize trade lanes, expand into new markets, discover alternative buyers and suppliers, as well as spot supply and demand shifts from a single integrated web-based platform to cost-effectively enhance your supply chain resilience and competitive edge.

Special Reports

2026 Top 30 U.S. Port Report

See how tariffs, routing choices, and sourcing strategies quietly reshaped the U.S. imports, and what those changes mean for 2026.

Download the 2026 Top 30 U.S. Port Report

A Year of Evolving U.S. Tariffs Reshapes Trade in Plastics

A surge in Transpacific plastic imports boosted U.S. port volumes in 2025, according to Descartes Datamyne™. Tariffs drove supply chain shifts for plastic goods, materials, and machinery.

Read the Report

An Analysis of U.S. Import Volumes Transiting Through the Strait of Hormuz

While the Strait of Hormuz accounts for a relatively small share of total U.S. maritime imports, the data shows that exposure is highly concentrated in critical commodities.

Read the Report

How Descartes Can Help

Descartes Datamyne delivers business intelligence with comprehensive, accurate, up-to-date, import and export information.

Our multinational trade data assets can be used to trace global supply chains and our bill-of-lading trade data – with cross-references to company profiles and customs information – can help businesses identify and qualify new sources. Ask us for a free, no obligation demonstration of our data on a product or trade commodity of your choosing – and keep the custom research we create with our compliments.